Analysis of the development status and prospects of China's dye industry in 2017

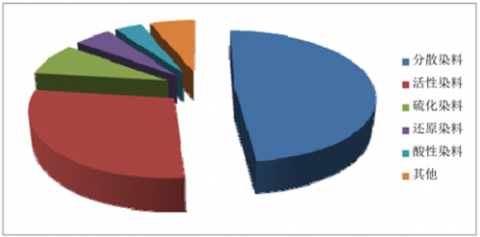

HC Chemical Network News: Dye Classification and Use Dyes are substances that can make fabrics or other substances dyed into bright and strong colors. According to its source, it can be divided into two major categories: natural and synthetic. Natural dyes are generally derived from plants, animals and minerals, and are mainly plant dyes such as indigo, valerian, comfrey, safflower, mulberry, and tea. Synthetic dyes, also known as artificial dyes, mainly from coal tar 1, dye classification and use Dyes are substances that make a fiber fabric or other substance a bright, strong color. According to its source, it can be divided into two major categories: natural and synthetic. Natural dyes are generally derived from plants, animals and minerals, and are mainly plant dyes such as indigo, valerian, comfrey, safflower, mulberry, and tea. Synthetic dyes, also known as artificial dyes, are mainly chemically processed from coal tar fractionation or petrochemical primary products. According to the different chemical structures of the dyes, the dyes can be classified into azo dyes, anthraquinone dyes, aromatic methane dyes, steroid dyes, sulfur dyes, phthalocyanine dyes, nitro and nitroso dyes, and the like. According to the nature of the dye and the application method, the dye can also be classified into disperse dyes, reactive dyes, sulfur dyes, vat dyes, acid dyes, direct dyes and the like. The main application fields of dyes are the coloring of various textile fibers. They are also widely used in plastics, rubber, ink, leather, food, paper and other industries, and play an important role in enriching people's material and cultural life. In recent years, the characteristics of dyes in optics and electricity are gradually recognized by people, and gradually penetrate into modern high-tech fields such as information technology, biotechnology, and medical technology. 2. Overview of the development of the dye industry (1) Development status of the international dye industry The downstream industries of the dye manufacturing industry are mainly the printing and dyeing sub-sectors in the textile industry. In recent years, with the development of the world textile industry and printing and dyeing industry, the world dye industry has maintained a steady growth trend. In the world dye market, since the mid-1990s, after several mergers and acquisitions, strong alliances, the three major global dye suppliers of DyStar, Huntsman and Clariant have been formed. It accounts for about 50% of the global market share. Since then, with the shift of the world's clothing, textile, fiber, printing and dyeing industries, the dye industry in China and India has made great progress and has gradually become the main production base of dyes in the world. At present, the development of the world dye industry is roughly as follows: 1 The world dye industry has completed its transfer to Asia, and China has become the world's largest dye production base. Since the mid-1990s, the global dye giants have set off a strong merger and reorganization. Bayer and Hoechst merged the dye business of both parties, the merger of DyStar and BASF dyes business, Huntsman acquired Swiss Ciba Refinery, Zhejiang Longsheng, India KIRI acquired DyStar, etc., the global dye industry production Concentration continues to increase. With the rapid development of the textile industry, the transfer of dye industry production and technology, and the acquisition of traditional international giants in the international market by large Asian companies, the dye industry in Asian countries has developed rapidly. Among them, China and India have the fastest growth, and a large number of large enterprises with strong production strength and strong R&D capabilities have emerged. At the same time that the world dye industry moved to Asia, competition among dye companies in China, India and South Korea, the major dye producing countries in Asia, began to appear. At present, China's dye production accounts for more than 65% of the world, and has become the world's largest dye production and supply base. The developed countries have gradually withdrawn from the basic dye synthesis business, forming a semi-finished dye product mainly imported from China and India to process high-value-added dye commercial products, or directly purchasing dye products from OEMs of both countries and OEM. Sales business model. 2 Green environmental protection requirements are getting higher and higher, and it has become an important part of the core competitiveness of dye companies. With the increasing awareness of environmental protection worldwide and the increasing requirements of environmental protection policies, environmental protection issues in textile and textile production are highly valued. Non-toxic, non-polluting "green fabric" has become a mainstream of textile production and consumption. In addition, dye products will be more widely used in plastics, rubber, ink, leather, food, paper information technology, biotechnology, medical technology and other fields, which also puts higher requirements on product technology and environmental protection. At present, the International Textile Ecology Research and Inspection Association has issued a new version of OEKO-TEX Standard 100 at the beginning of each year, and the REACH Regulations promulgated by the European Union have put forward high requirements for the environmental protection of textile dyes. This aspect has increased the cost of developing new textiles and dyes, and on the other hand will promote the transformation of dye products into a green environment. Dye companies that cannot achieve green environmental protection and can't make large investments in environmental management will be eliminated in the fierce market competition. 3 product features, enrichment will get more attention from dye companies With the continuous development of the world economy, the consumption of international textiles presents a trend of market, variety, style, color and diversity and advocating natural environmental protection. The continued growth of the economy has increased the purchasing power of consumers, and the demand for personalized, comfortable, branded and fashionable textiles has also increased. At the same time, various new fiber and blended fabric products have emerged to cater to consumption. The special needs of the person. This will drive the demand for dye products with better dyeing performance and characteristic dyeing to grow rapidly, and the variety of dye products will be more abundant. (2) Development status of domestic dye industry 1 market situation Since the reform and opening up, especially after the 1990s, with the transfer of the world's clothing, textile, fiber, printing and dyeing industries, the rapid development of China's dye industry has been driven. The output of the dye manufacturing industry increased from 257,000 tons in 2000 to 922,200 tons in 2015. During the “Eleventh Five-Year Plan†period, the output of China's dye industry remained between 67-76 million tons, accounting for about 70% of the world's total; the export volume of dyes remained at around 230,000-280,000 tons. During the “Twelfth Five-Year Plan†period, the dye industry continued to maintain a steady growth trend. In recent years, China's dye industry output (unit: 10,000 tons) data as shown below: Unit: 10,000 tons China currently produces about 600 kinds of dyes, covering all major dye categories, which can meet most domestic market demand. In 2015, the order of dye production in China was disperse dyes, reactive dyes, sulphur dyes, vat dyes, acid dyes, etc. The specific yields were as follows: Disperse dyes are the most important of all dye classes. According to statistics, in 2012, the global production of polyester fiber (polyester) reached 41.4 million tons, accounting for the largest proportion of all fiber production in the world, 48.25%, and the only dyeing and printing on polyester fiber (polyester) It is a disperse dye. At present, disperse dyes have the highest yield and the largest export volume among all varieties of dyes in China. In 2015, China's disperse dye production was 447,100 tons, accounting for 48.49% of China's total dye production. At present, the types of disperse dyes produced in China are relatively complete, including azo, anthraquinone and heterocyclic. Among them, azo is about 75%, oxime is about 20%, and heterocyclic is about 5%. The disperse dyes are mainly azo. Disperse dyes with azo structure have short production cycle, high yield, low price and complete chromatogram, which play an important role in disperse dyes, accounting for about 75% of the total amount of disperse dyes. Bright color, good leveling, resistant to sun, wash, acid and alkali, perspiration and so on. Reactive dyes are the second largest dye variety other than disperse dyes. In 2015, China's reactive dye production was 263,300 tons, accounting for 28.52% of China's total dye production. At present, China's reactive dye market is in a transitional phase from decentralization to concentration. The most important manufacturers are Zhejiang Longsheng, Bauxite and Jiangsu Jinji Industrial Co., Ltd. The issuer has strong production and technical advantages in the field of important acid H-acids necessary for the production of reactive dyes. Therefore, it also has strong market competitiveness in the reactive dye market. In recent years, China's sulphur dye production ranks third among domestic dyes. In 2015, the industry's sulphur dye production was 74,700 tons, accounting for about 8.10% of China's total dye production. The main producers of sulphur dyes are Shanxi Linyi Dyeing (Group) Co., Ltd., Tianjin Dyeing Chemical Co., Ltd. and Inner Mongolia Yabulai Dyestuff Co., Ltd. The market for sulphur dyes in China is also at a mature stage, and domestically produced sulphur dyes can basically meet the needs of domestic printing and dyeing enterprises. 2 Development characteristics of domestic dye manufacturing industry At present, the characteristics of domestic dye manufacturing mainly include: A. The number of dyes produced, exported and consumed ranks first in the world. With the rapid development of the textile industry, the transfer of dye industry and technology, environmental protection, technology update and other factors, the global dye industry has undergone a major change since the beginning of the 21st century. China has become a world dye. Production and supply centers, China's dye production, exports, consumption, both ranked first in the world. In 2015, the total output of dyes in China reached 922,200 tons, the export volume was 253,000 tons, and the internal sales volume was 669,000 tons. From 2010 to 2015, China's dye production increased by an average of 4.05% per year, and the export volume remained between 243,500 tons and 290,200 tons. B. The scale of advantageous enterprises is continuously expanding, and the concentration of industries is further improved. After years of market competition and continuous elimination and integration, the concentration of dye production in China is constantly improving. Enterprises with scale, technology, capital and first-mover advantages in the industry, such as Zhejiang Longsheng, Bauxite, and issuers have all developed. The enterprise group with annual sales of several billion yuan, the total output of dyes of Zhejiang Longsheng, Bauxite and the issuer has been ranked among the top three dyes in the country for many years and has become a world-class dye company. In addition, Yabang, Shanxi Linyi Dyeing (Group) Co., Ltd., Tianjin Dyeing Chemical Co., Ltd., etc., these enterprise groups also have relatively strong capital and strong market operation capabilities. C. Environmental protection policies are becoming more and more strict, and environmental protection is imperative. During the “Twelfth Five-Year Plan†period, the state put forward more stringent requirements on the dye industry in terms of environmental protection. With the promulgation and implementation of the environmental law known as "the most severe in history", the environmental pressure of the dye industry is increasing. In recent years, the increasingly strict environmental protection policies have directly affected the production capacity of some enterprises. A large number of small and medium-sized enterprises lacking environmental protection investment have shut down production capacity or suspended production. Therefore, environmental protection upgrades for companies in the dye industry are imperative. The development of green environmental protection in the dye industry should not only focus on the greening of its own production process, but also increase the management of “three wastes†and continuously promote the application of cleaning processes. At the same time, it should also pay attention to the environmental protection of dye products and accelerate through technological progress. Development and research of green and environmentally friendly new products, and adjustment of product structure to enhance the sustainability of corporate development. D. The “going out†strategy has been launched and the international operation has achieved initial results. With the development of global trade liberalization, the accelerated implementation of the “going out†strategy by domestic dye companies has become an inevitable requirement for the development of China's dye industry. On the one hand, in recent years, China's dye exports have been maintained at 243,500 tons to 290,200 tons, accounting for 27.43% to 36.09% of China's total dye production. Therefore, the development and maintenance of overseas markets The development of the domestic dye industry is extremely important. Multinational operations can further understand the market conditions of the international market, and can also solve the problem of timeliness and cost of after-sales service for overseas customers. On the other hand, some large-scale dye companies in China also have the conditions to go global, such as the accumulation of capital and the mastery of environmental protection technologies. At present, Zhejiang Longsheng, a leading enterprise in the industry, has set up a special overseas operation platform. Through overseas mergers and acquisitions, it has obtained a controlling stake in the former world dye giant DyStar and has established a new dye production base in India and other places. E, product quality continues to improve, brand building results are significant In recent years, the quality of dye products in China has been greatly improved, especially in the aspects of synthetic technology and commercialization technology, and the quality of some products has reached the international advanced level. At the same time of improving quality, brand building has been highly concerned by large enterprises in the dye industry. Relevant enterprises have increased brand promotion through various forms such as international exhibitions, international conferences, advertisements, and media campaigns. F, the overall technical level of the industry is not high, and the innovation ability is weak. At present, low-end and general-purpose products in China's dye products account for a relatively high proportion, while the proportion of high-end and special-purpose products is relatively low. On the one hand, high-end products can not meet market demand, have to import high-priced or foreign-funded enterprises occupy the high-end market; on the other hand, homogeneity is widespread, and the characteristics of various production enterprises are not obvious. Technological innovation is a costly job, and the industrialization process is slow. In particular, the original dye innovation is a high-input, high-risk, high-return, long-cycle system engineering. Although in recent years, domestic dye companies have attached great importance to technological innovation, increased capital investment and invention patent applications, and made some progress, but the vast majority of small and medium-sized dye enterprises still have weak technological innovation capabilities. G, high performance, high value-added products rely on imports Although China's dye production, export volume and consumption rank first in the world, the proportion of product structure is still dominated by medium and low-end products. As the income level of the people has increased, market demand has changed and the demand for high-grade dyes has increased. During the “Eleventh Five-Year Plan†period, China imported about 40-60,000 tons of high-performance and high value-added dyes every year. H, product structure is not reasonable, technical innovation still needs to be strengthened In recent years, China's dye industry has significantly improved in terms of product quality, stability, and commercialization technology, but the product structure is still not reasonable. Most of the products are conventional varieties with low added value, and products between conventional manufacturers. The phenomenon of homogenization is more serious and lacks characteristics. The production capacity of some product varieties has increased too fast, and there has been a situation of overcapacity. Therefore, enterprises in the industry must regard technological innovation as the cornerstone of enterprise development in order to achieve the development goal of expanding the market and maximizing profits. On the one hand, we should start from improving product quality and expanding product categories, avoid vicious competition of similar products, and realize individualization, differentiation, high performance, and environmental protection of products. On the other hand, we will actively promote the construction of technological innovation systems with enterprises as the mainstay, research institutes as the support, market-oriented, products as the core, and production, education and research, and enhance the R&D technical personnel reserve and technical process reserves of the entire industry. The technology development and innovation system of the whole industry has changed from imitative development, follow-up innovation to creative development and original innovation. Editor in charge: Chen Xiaohui Chenille Fabric,Chenille Material,Polyester Chenille Fabric,Chenille Fabric for Clothing Jiangyin Xiangxu Textile Co., Ltd. , https://www.xiangxutextile.com